What the June BTO results reveal about how Singaporeans really choose their homes

I know someone who will walk two extra blocks for noodles that are 50 cents cheaper, and who only goes to town when a buddy can give him a ride.

Yet a few years back, this same person paid the highest price for their four-room flat in the area they live in.

Next year, this individual plans to upgrade to a five-room flat that is closer to their office.

It’s not a huge difference in travel time — perhaps just around three stops closer by train.

So what does this have to do with the recently concluded June 2026 BTO flat applications and HDB resale prices?

I think there’s a fair bit to take away from my acquaintance’s mindset and the demand for new BTO flats in the latest sales exercise.

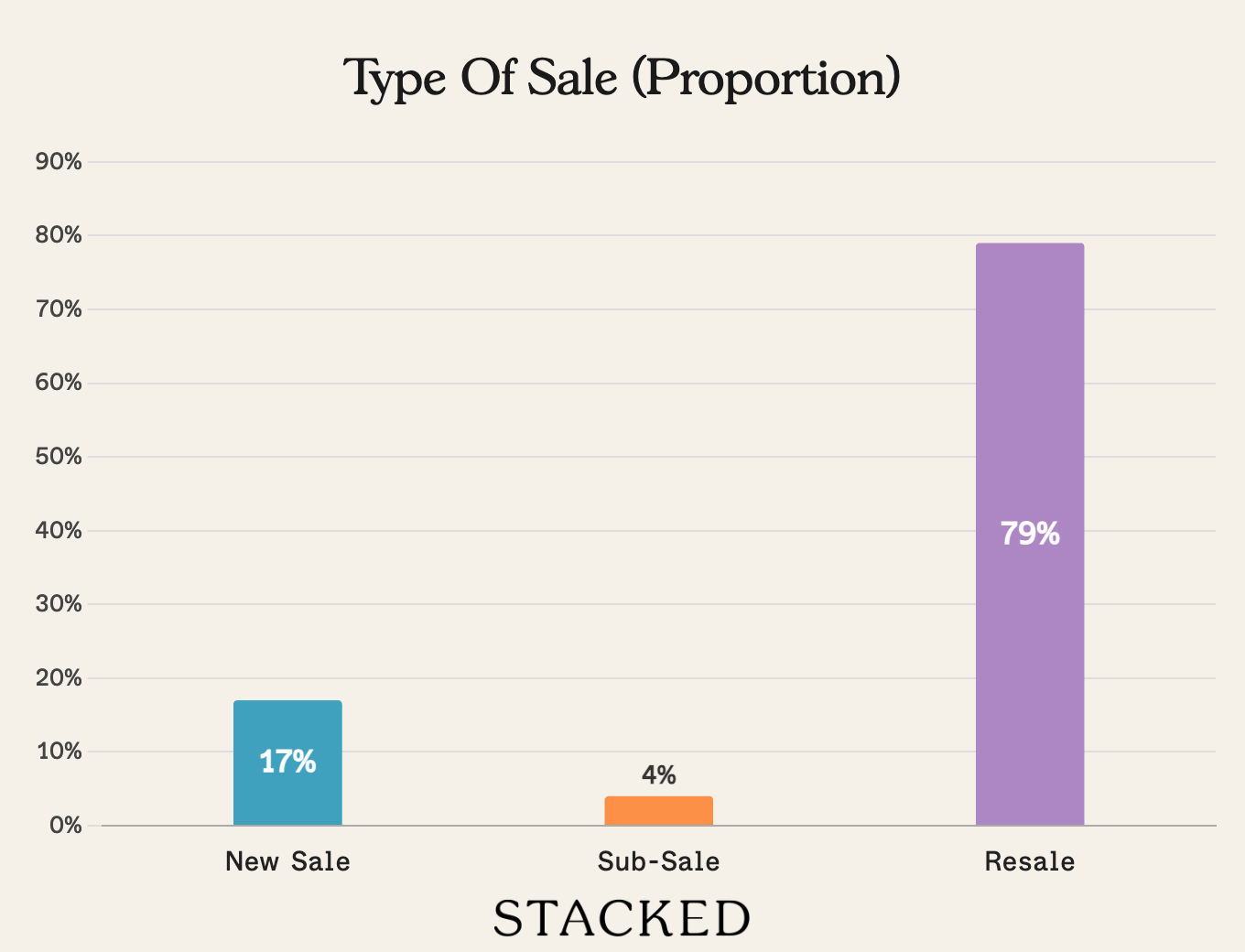

We reported that the sales exercise drew over 22,3 applications for 6,952 flats, which we covered in this article here.

We saw that two Prime projects — Berlayar Rise and Lakeview Cascadia — accounted for around 65per cent of all applications. Meanwhile, the two Standard projects in Sembawang were undersubscribed among first-timer families.

These weren’t typical Standard BTO projects — they came with a shorter build time of under three-years. However, application rates were just 0.7 for three-room flats, 0.6 for four-room flats and 0.4 for five-room flats.

Regardless, most of the interest among BTO applicants went toward the Plus and Prime flats.

These are pricier, will take longer to build, and come with restrictions that go way beyond a 10-year MOP.

But the high application rates indicate that most BTO owners are willing to accept that, along with the heftier price tag.

Let’s consider the new four-room BTO flats. Buyers could have applied for a four-room flat at Sembawang Brook that would be priced from $302,000, or at Woodgrove Acres that starts from $353,000.

Instead, we saw that a relatively large proportion of the demand flowed toward Lakeview Cascadia, where four-room flats start from $534,000, and Kebun Baru Ridge where these units are priced from $543,000, as well as Berlayar Rise which sees prices from $592,000.

(For a thorough review of all the projects in this sales exercise, see our June BTO launch guide).

That’s a premium of roughly $180,000 to almost $300,000 before grants.

Yet these projects still attracted the lion’s share of applications, despite longer waiting times and significantly tighter resale restrictions.

This is in stark contrast with some Singaporeans who I have met over the years.

Most are eminently practical and willing to go far to preserve their savings, but when it comes to housing — just as with their children’s education apparently — the restraints loosen.

It appears that these same reasons drive the behaviour of my acquaintance.

When it comes to housing, affordability matters. But that’s not the same as simply going for the cheapest option; it’s about looking for the biggest improvement that they can realistically afford.

[[nid:738611]]

I’m not entirely sure. I acknowledge the possibility that some Singaporeans have underestimated the impact of Prime and Plus restrictions.

As I pointed out previously, many buyers seem to focus on just the 10-year MOP and Subsidy Recovery.

I notice fewer buyers focus on the resale income ceiling and Mortgage Servicing Ratio (MSR), which will also apply to future buyers.

Along with the Subsidy Recovery and almost 13-year total wait time, Plus and Prime projects have built-in mechanisms that dissuade windfall seeking owners.

That said, I think it’s more likely that most buyers at least understand the broad trade-offs.

Some may be underestimating the degree of the effect, but in general they know they’re accepting significant drawbacks.

And yet, many have consciously decided the trade-offs are worth the while.

Their day-to-day quality of life, from being in a more convenient location, may come ahead of resale gain or property progression.

If Singaporeans value location, convenience, and quality of life above room for price growth, upgrading, etc., then it also explains why it’s so hard for resale flat prices to dip — even if there’s higher supply in the market.

Over the past year, the HDB resale market has seen much more supply. Around 13,480 flats are expected to reach their MOP this year, almost double last year’s 6,973 units.

The public housing market has also improved since the end of the Covid-19 pandemic.

We went from a scene where new housing supply couldn’t keep up with demand, to a situation where the overall supply has matched long-term demand trends.

And yet in the first three months of this year, about a third of resale buyers still paid at least $800,000 for their flats, and million-dollar transactions continue to climb.

The broader resale market may be cooling, but demand for the most desirable locations remains unshakeable.

The overwhelming demand for Plus and Prime flats may simply be another expression of the same mindset we already see in the resale market.

When given a choice, many Singaporeans will pay a substantial premium for a home that better suits them.

If a million-dollar resale price ever follows, that’s welcome. But perhaps for an increasing number of buyers, that’s a secondary benefit.

[[nid:738611]]

In our analysis last year, we found that many 50-year-old flats in mature estates continued to sustain high prices.

Older five-room flats in Toa Payoh still saw average prices of above $1 million in 2025, while similarly aged units in Marine Parade recorded average prices of around $938,000, and Kallang/Whampoa around $765,000.

Even four-room flats in Queenstown, Marine Parade and Bukit Timah continued to transact comfortably above the $600,000 mark.

If a substantial number of Singaporeans aren’t even afraid of lease decay, despite the end of Sers, then a 10-year MOP, Subsidy Recovery, and income ceiling scare them even less.

Whether this was the government’s intention or not, it seems to me that the introduction of Plus and Prime flats may have ended up doing more than just preventing unfair windfalls.

It created a system that reveals a big part of the Singaporean homeowner’s psyche towards home ownership.

These rules deliberately make these flats less attractive to buyers chasing gains, yet we find many Singaporeans still rushing for them.

At the same time, we can see on the tail-end that prices of central area flats — in their last 50 years of existence — defy gravity and continue to draw interested buyers.

Put the two together, and it contours a very common online complaint: that Singaporeans keep using HDB flats as investment assets. In reality, all the behaviour so far points in the opposite direction.

Resale flat prices are expensive precisely because most Singaporeans prize home ownership over yield, capital gain, or other spreadsheet calculations.

Persistently high resale prices may not simply suggest that Singaporeans treat public housing as investment assets.

It may reflect something much more mundane: We’re willing to pay a premium to live where we genuinely want to live.

And we’re willing to do so regardless of Plus and Prime restrictions, or lease decay.

[[nid:738131]]

Project name Price S$ Area (sqft) $PSF Tenure

River Modern $6,180,000 1830 $3,377 99 years (2025)

One Marina Gardens $5,418,000 1647 $3,290 99 years (2023)

The Continuum $5,330,000 1905 $2,798 FH

J’den $3,751,000 1485 $2,525 99 yrs

Canninghill Piers $3,613,000 1130 $3,197 99 yrs (2021)

Project name Price S$ Area (sqft) $PSF Tenure

Narra Residence $1,542,000 700 $2,204 99 years (2025)

Coastal Cabana $1,670,000 915 $1,825 99 years (2024)

Bloomsbury Residences $1,720,000 678 $2,536 99 years (2024)

Hudson Place Residences $1,765,000 689 $2,562 99 years (2025)

Canberra Crescent Residences $1,995,861 990 $2,015 99 years (2024)

Project name Price S$ Area (sqft) $PSF Tenure

Hilltops $8,088,600 2379 $3,400 FH

Draycott Eight $7,500,000 2906 $2,581 99 years (1997)

The Draycott $5,650,000 2637 $2,142 FH

Palm Spring $4,360,000 1862 $2,341 FH

Leonie Gardens $4,200,000 2540 $1,653 99 years (1990)

Project name Price S$ Area (sqft) $PSF Tenure

River Isles $720,000 441 $1,631 99 years (2012)

Skysuites17 $735,000 377 $1,951 FH

EuHabitat $755,000 538 $1,403 99 years (2010)

Space @ Kovan $783,666 549 $1,428 FH

Treescape $793,000 431 $1,842 FH

Project name Price S$ Area (sqft) $PSF Returns Holding period

Leonie Gardens $4,200,000 2540 $1,653 $2,930,000 28 Years

The Esta $3,388,888 1346 $2,519 $2,464,278 20 Years

Mirage Tower $3,700,188 1496 $2,473 $2,370,188 20 Years

Blossoms @ Woodleigh $2,768,000 1206 $2,296 $1,993,000 19 Years

Gold Coast Condominium $3,200,000 1894 $1,689 $1,800,000 17 Years

Project name Price S$ Area (sqft) $PSF Returns Holding period

Marina Collection $2,780,000 1873 $1,484 -$2,167,760 18 Years

Reflections at Keppel Bay $4,050,000 2336 $1,734 -$782,100 19 Years

Robinson Suites $1,155,000 506 $2,283 -$565,000 16 Years

OUE Twin Peaks $1,175,000 570 $2,060 -$394,100 10 Years

Marine One Residences $1,270,000 753 $1,686 -$347,145 Six Years

Project name Price S$ Area (sqft) $PSF ROI (per cent) Holding period

Braddell View $1,541,688 1453 $1,061 267per cent 20 Years

The Esta $3,388,888 1346 $2,519 267per cent 20 Years

Blossoms @ Woodleigh $2,768,000 1206 $2,296 257per cent 19 Years

Leonie Gardens $4,200,000 2540 $1,653 231per cent 28 Years

The Tessarina $2,400,000 1033 $2,323 216per cent 22 Years

Project name Price S$ Area (sqft) $PSF ROI (per cent) Holding period

Marina Collection $2,780,000 1873 $1,484 -44per cent 18 Years

Robinson Suites $1,155,000 506 $2,283 -33per cent 16 Years

OUE Twin Peaks $1,175,000 570 $2,060 -25per cent 10 Years

Marina One Residences $1,270,000 753 $1,686 -22per cent Six Years

Reflections at Keppel Bay $4,050,000 2336 $1,734 -16per cent 19 Years

[[nid:738918]]

This article was first published in Stackedhomes.

……Other

One-stop lifestyle app dedicated to making life in Singapore a breeze!

English

English 简体中文

简体中文

Comments

Leave a comment in Nestia App